Bottom-line Winners – Junk-Pile Trades

15% of my trades –

At the end of the year, these special trades are all that matter. These are the BOTTOM-LINER trades.

85% of my trades –

At the end of the year, the results of these trades just do not matter, but how they are managed matter much. These are the JUNKPILE trades.

Part 1 – Trading against expected metrics

As a trader I have always been interested (one might say “obsessed”) with data. I view myself as a data-driven trader. I am incredibly fortunate to have kept data on many aspects of my trading since founding Factor Trading Co., Inc. at the Chicago Board of Trade in 1981. This abundance of data provides me with a deep understanding of numerous benchmarks and metrics of my trading and risk management protocols. I did not begin collecting data thinking that someday the data would become extremely valuable in understanding the dynamics of a trading program – I collected the data because I have always loved data. Nevertheless, the data have become precious.

Since the inception of Factor I have remained primarily a classical chartist. Yet, the prism through which markets are viewed is one thing – actual trading tactics are an entirely different thing. While continually a chartist, my trading tactics have evolved through the years for various reasons (subject of another day). By tactics, I mean such things as:

- Entry techniques

- Time frames for market analysis

- Expected holding time for trades – wins vs. losses Trading frequency

- Risk management protocols

- Sizing and leverage considerations

- Trade management techniques and rules Order management

- And, a host of other things

During the 1980s and early 1990s, I traded approximately 25 to 30 signals per month. From the mid-2000s through early 2014, I traded about 20 signals per month. Since early 2014, I have thought more in terms of trading themes than individual trading signals – in reality, I may have several signals in a given market under the umbrella of the same trading theme. My view of a “trade” is broader now than it was in the past. From early 2014 throughthe present I have been engaged in about 8 to 10 trades (themes) per month. My goal is to move toward only five themes per month.

How do I define a trading theme? This question is best answered by some recent examples. In my mind, long Silver and long Platinum were expressions of one trade, long Meal and long Beans were part of one trade and two attempts at long GBP were part of the same trade.

My profit goal is 35% per year – knowing that some years will greatly exceed this figure and losing years are possible. My goal is to move toward 50 trades per year. Let’s use the 50 trade figure as an example for a case study.

Based on my historical benchmarks, 50 trades will result in the following:

- 21 trades (42% of all trades) will produce a profit

- 8 trades (15% of all trades and 36% of the profitable trades) will produce the net bottom line (thus, I refer to these trades as “bottom-liners”)

- 13 trades (21 minus 8) will be “lesser” profitable trades

- 29 trades (58% of all trades) will be losers

- Thus, for the 8 “bottom-liners” to represent the net profit, the 29 losing trades must be offset by the 13 lesser profitable trades

Let me translate the data above into basis point equivalencies. Remember, 100 basis points (BPs) equals 1% of total nominal trading capital.

- 8 “bottom-liners” need to produce an average profit of 450 basis points (8 times 4.5% = 36%)

- Assume the 29 losing trades will average minus 36 BPs, or a total of minus 1044 BPs. Question – How many of you have lost 10% of your trading capital in just one trade?

- This means that the 13 “lesser” profitable trades need to achieve an average profit of 80 BPs to offset the 29 losers – and, thus, allow the 8 “bottom-liners” to produce the net result

Assume that I trade an average of 8 futures contracts per $1M of nominal capital. [Keep in mind that the actual size – depending upon the market traded and the specific chart set up – may range from 3 to 25 contracts per $1M of capital.] The equivalent size in spot forex would be a position valued at approximately $800,000 per $1M of nominal capital (even if the USD is not a pair within a specific forex trade).

Let me now translate this data into the USD result per futures contract (or spot forex equivalent as cited above).

- The 8 “bottom-liners” must produce a profit of $5,600 per futures contract (or FX equivalent)

- The 29 losing trades must be limited to minus $450 per contract (or FX equivalent)

- The 13 “lesser profitable” trades must produce an average profit of $1000 per contract (or FX equivalent)

In my experience, there are only two tactical solutions to produce the data above:

- Let winners run – cutting winners prematurely would make it nearly impossible to achieve eight trades at 450 BPs each. Yet, certain persuasions are necessary to prevent winning trades from becoming “popcorn” trades.

- Aggressively advance stops on any trade that hesitates, thus “scratching” trades that could become 50 to 60 BP losers. Of course, in the process some potentially large winning trades might be jettisoned too early, but this is the trade-off I am willing to make to protect capital as Job #1.

Let me unpack item #2 above in more detail. A trade with an initial risk of 60 BPs (see Tracking Account spreadsheet for examples) represents a stop of about $750 per futures contract (or FX equivalent). My job as a trader is to shrink this potential loss as quickly as possible. To do so, I must attempt to adjust my risk level within a day or two after trade entry. The goal is to move stops to insure a break-even trade within a week.

Summary

I really want all Factor members to understand this concept – my real focus is the 15% of trades that hopefully establish a profitable bottom line at the end of a year. I refer to these as BOTTOM-LINE TRADES. This means that 85% of my trades are throw away trades – or, what I refer to as JUNK-PILE TRADES. This concept explains why an individual trade is relatively unimportant to me. An individual trade is simply a data point in a series of data points. It is unimportant if a trade is a profit or loss as long as:

- It is based on chart configurations meeting certain standards

- The leverage and trade management of the trade comply with predetermined guidelines

- In other words, stick to the basics, focus on process and let profits take care of themselves

Factor Membership

This was Part one of a three part series, titled: Bottom-line winners and junk-pile trades

Part 2 of this series focuses on Bottom Liners.

Part 3 of this series focuses on the Junk Pile of lesser profits and losers.

Part 2 and 3 are available to members of the Factor Service only.

Factor Membership is available. For more information watch my 30 minute webinar where we cover the Factor service in depth.

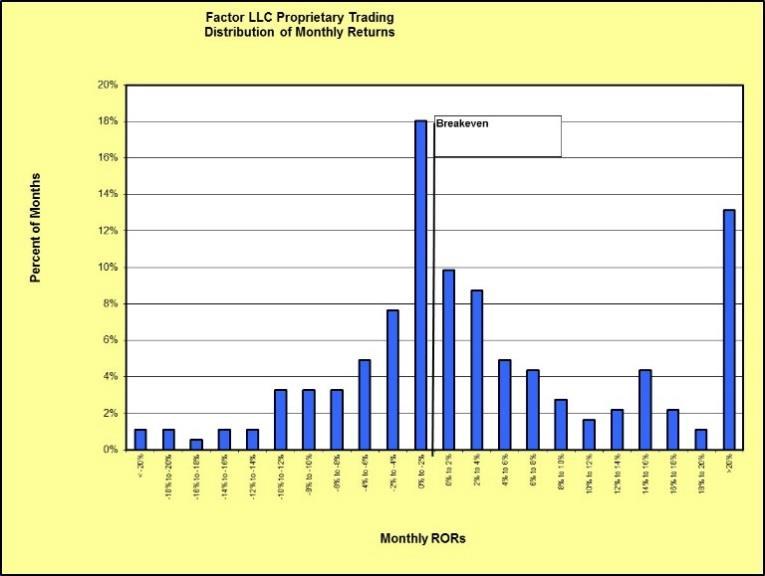

Distribution of monthly RORs

Different approaches to trading should result in different statistical profiles. The graph below displays the distribution of the Factor’s monthly RORs over the years. The distribution of monthly RORs shown on the graph are very consistent with the summary of Factor’s trading strategy and tactics explained on the previous page.

- A small percentage of trades (15%) producing the net profitability should produce a large right-handed outlier. This is exactly what the monthly distribution of RORs shows.

- The most common month should be a small loser with the majority of trades (59%) being losers. This is exactly what the monthly distribution of RORs shows.

In an average year (keeping in mind that an average year is a statistical event – in reality, there are no average years), five months will be breakeven months (-2% to +2%), three months will be losing months (>-2%) and four months will be winning months (>+2%) of which one to two months will reside in the right-handed outlier column.

The profile of monthly RORs will be very different for different trading approaches. For example, short-term mean reversion trading approaches typically will not have right- or left-handed outliers, but will squeeze into the middle with the highest column being a small winning month.

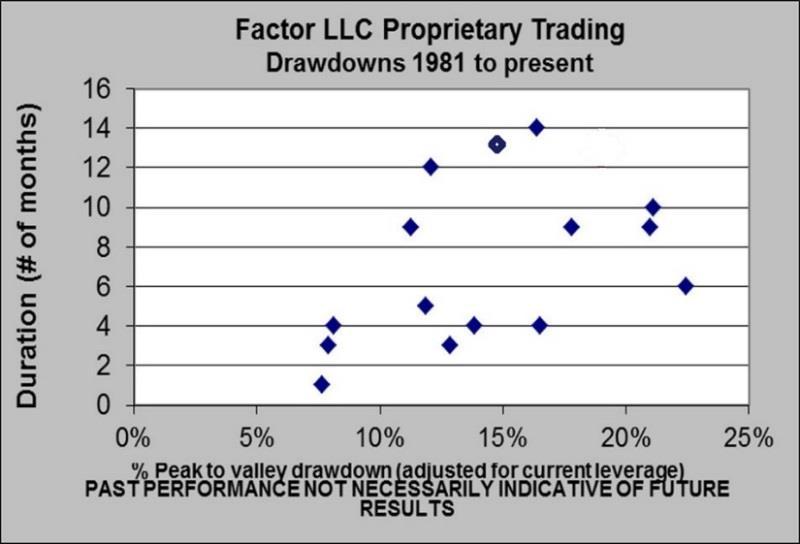

Drawdowns

Drawdowns are an inevitable part of trading. There are some industry-accepted metrics related to the expectation of drawdowns for discretionary traders such as myself. Drawdowns must be taken into account when analyzing risk-adjusted performance.

The investment industry is obsessed with the Sharpe Ratio – which is, in my opinion and the opinion of most other proprietary traders I know – about the most worthless measure of trading performance invented by mankind. The fact the investment community is so obsessed with Sharpe is a confirmation of the lack of sophistication within the wealth management industry seeking to “manage” the capital of private investors. The best source of information on trading metrics can be found in Jack Schwager’s book, “Market Sense and Nonsense.”

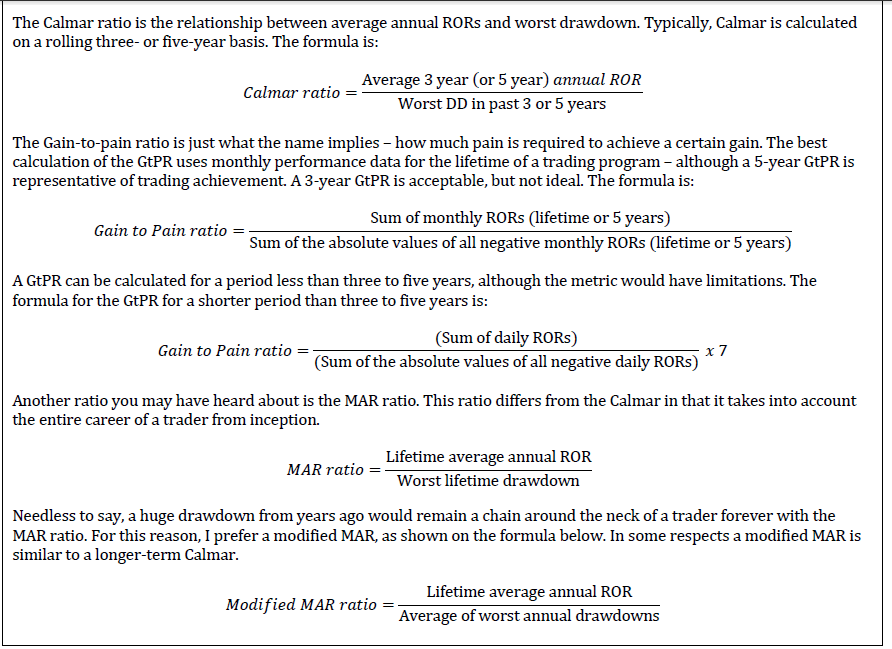

There are two metrics I consider to be most important in appraising risk-adjusted performance – the Calmar ratio and the Gain-to-Pain ratio.

For both Calmar and Gain-to-pain ratios, a value greater than 1.0 is considered to be quite good, above 1.5 is considered to be very good, above 2.0 is considered to be excellent, above 2.5 is excellence-on-steroids, and above 3.0 is world class. Anything above 1.0 to 1.5 for MAR is excellent.

Based only on audited years, the Factor’s MAR is 1.3, modified MAR is 2.6, and GtPR is 2.5. Calmar is a metric that all traders should be aware of because it places upside performance into a proper perspective. A rolling Calmar of 1.5 (which is very good) suggests that a trader seeking a performance of 24% per year should expect annual drawdowns in the area of (16%).

Drawdowns are the curse of a trader. I have been through many drawdowns in my career and they do not get easier. The challenge of a trader is to ride through these drawdowns, preserving both financial and emotional capital. To do so, a trader must constantly remained grounded in the foundational truths of his or her trading program.

Foundational truths include some of the following aspects:

- Complete self-transparency and honesty (or, as near complete as is humanly possible)

- Intimate knowledge of one’s trading program in all respects – trade signaling, risk and trade management

- Knowledge of how one’s trading program should perform in different types of market environments

- Statistical measurements to provide guidance as to whether a trading program is “going off the rails”

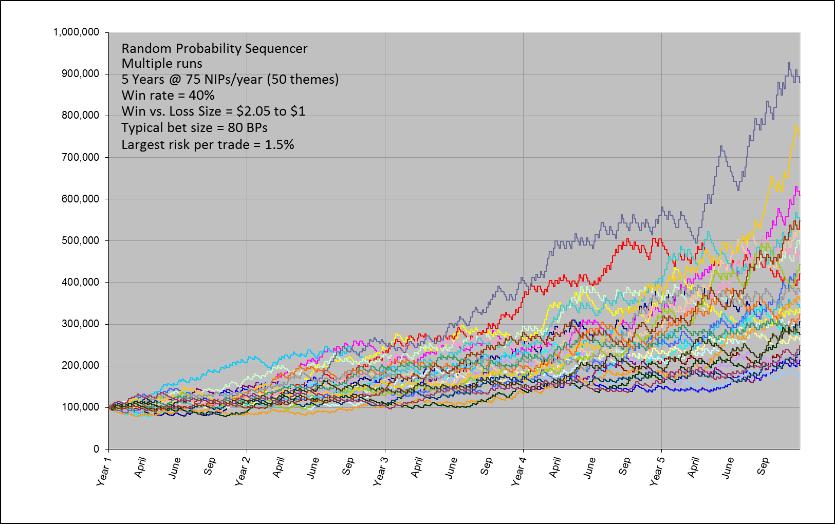

The longer a trader has traded a basic approach (allowing for some evolution along the way), the more intimate a trader will become with his or her trading approach and its moods and inclinations. I have a huge advantage on this score, having traded classical patterns for a living since 1981. I have both an instinctual and statistical sense of my trading approach. When N equals a large number (N being the number of trading events experienced by a trading approach), statistical benchmarks become more stable. My benchmarks are quite stable when projected over a multi-year time frame. The graph below displays a NAV over a five year period produced by a random-number generator. I have run thousands of sequences since being part of the small group of traders who developed the Excel program used to perform this analysis. The graph below shows only 30 sequences.

Statistically I also know the probabilities of various drawdowns. For example, I know that annual drawdowns of approximately minus 9% to minus 17% have a probability within a single standard deviation. The table below is based on my historical benchmarks. I have made some changes in the past two years to trade management protocol in an attempt to push the skew of the STDs to the left. Exploration aimed at this goal continue.

I completely understand that many of you do not have a solid grasp on the statistical probabilities of their trading approaches – and, in fact, too many Factor members do not even have a firmly articulated trading plan. This is why I encourage developing traders to go slow. Bet small, have realistic expectations and make capital preservation Job #1 until some of these other facets of trading gain clarity.

Factor Membership

This was Part one of a three part series, titled: Bottom-line winners and junk-pile trades

Part 2 of this series focuses on Bottom Liners.

Part 3 of this series focuses on the Junk Pile of lesser profits and losers.

Part 2 and 3 are available to members of the Factor Service only.

Factor Membership is available and you could consider your membership in the Factor Service as just one more trade. If the Factor Service is not of value to you, well, it is just one more trade that did not work. Through the Factor Service I endeavor to alert novice and aspiring traders to the many pitfalls you will face – and to offer advice on overcoming those pitfalls. My goal is to shoot straight on what trading is all about. For more information watch my 30 minute webinar where we cover the Factor service in depth.

I hope you will consider joining the Factor community.